INTRODUCTION

This page had been maintained by Ekin Sarıyıldırım, Gökberk Bilgin

and Ipek Korkmaz as a part of the project studied during ECON

318 lecture at Bilkent University for the spring 2018 semester. All the

information gathered here are from external sources; we try to give the source

of information as much as we can.The opinions expressed in this work are

solely unbiased analysis of the work rendered. This project explores the

possibility whether a “trading center” and/or “pricing location” for MED

(Mediterranean) diesel deliveries in Turkey is economically and technically

feasible. The exercise is based on the feasibility study of a trading center that is importing diesel either from the

East of Suez. As a practical and reliable approach, Jamnagar and Jubail are

taken as two reference points both with potential and keen to export diesel in

MED market. This is an interesting

exercise to conduct since in case of its application; it will increase the energy supply security of Turkey and could

create competitive advantage to the supplier counterparties. Additionally, the new

deals linked to this route could provide discounts on the diesel purchases, and Turkey may profit from the storage

facilities that are planned to construct. The information that is used here is valid by May 21, 2018.

TECHNICAL ASPECT

When the crude oil is

processed, it yields different products; diesel (or gasoil)

is also a product that has to be produced by the refineries through to the crude

oil processing. How

much each of these products produced is determined

by various factors such as the complexity of refineries, the type of crude oil refined

and the economy of the products in the market. The quality of these products

may differ as to the configuration of the

refineries change.

Even though there are some restrictions towards

the diesel consumption in European countries, the diesel demand will rather increase. Turkey is one of the largest importers of

diesel/gasoil in the global market. USA and Russia are the biggest exporting

countries, alongside

the other major players. India and Saudi Arabia are some of the major

suppliers for MED because of their refinery configuration, product

specifications and the proximity to the market. Thus, India’s and Saudi Arabia’s continuously increasing

refinery capacities can supply additional

volumes of ultra-low sulfur diesel that meets the Europe’s demand. As a result,

the volume of diesel/gasoil trade is growing. Turkey’s location and its local

demand could create a potential for the diesel/gasoil trade from the East of

Suez to Southern Europe to be carried via Turkey; Mersin port for our base

scenario.

Clean vessels (also known as

clean tankers) are the core part of the diesel/gasoil physical trade. The specification of a vessel depends on many different factors,

such as the distance between the trading

locations and cargo size. These vessels usually move on specific trade routes.Our project’s main focus is the

diesel/gasoil trade from the East of Suez to MED via Mersin, Turkey, we have analyzed the cost of a diesel/gasoil vessel for two cases; the vessel stops either at

Mersin Port, or direct shipping to the

consumption location i.e. Southern Europe. For our calculations, it is worth bearing

in mind that we use some certain methodology and assumptions.

To calculate a vessel’s voyage cost,

some assumptions have been made. Suez Canal

Cost is added for the routes that are starting from

India or Saudi Arabia since for the

vessel to arrive at Mersin, it must pass the Suez Canal. We are further

assuming that the diesel/gasoil is staying in the storage facility, in port

of Mersin,

according to the demand of the importing countries.

To understand

whether this operation is feasible or not, we have developed several

scenarios. We have simulated how a trade would be profitable if

there was a diesel/gasoil storage area in Mersin. In one of our simulations, we have assumed that Turkish state

will have a diesel/gasoil storage facility and they will re-export to Europe

during contango periods. Our findings showed that due to the price differences

between Arabian Gulf and Mediterranian if

Turkey sells with current prices, it might

face losses. However, in the long-run, if

Turkey can become a trading and price reference point for the region, it will

have the power to price the products

according to regional demand.

In the second analysis, we have assumed that the storage facility

belongs to either India or Saudi Arabia, or both of them. We have checked the

average trade to each European country from India and Saudi Arabia. In the case where India owns the storage, our

findings showed that by increasing the diesel/gasoil amount that is supplied to Turkey, a storage facility could be

operated and the stored diesel/gasoil can meet the demands of France

with a more profitable way and the transportation time will reduce 66%. If the aforementioned case is not profitable and

European countries do not choose to buy from Mersin, the stored diesel/gasoil can

be used domestically as well.

Overall, the

results show that main issue of becoming a hub is understanding the pricing mechanism

and finding a way to control it in order to

gain profit. Transportation and storage are also essential elements. Since the diesel/gasoil producers and transporters are not from the same company

or same country, building a model where every party involved win is pretty

hard.

In our simulation,

we have used both spot prices and forward curvess separately. Also, even though

we have assumed countries to own the storage facilities; in real life, private

companies and traders own them. Therefore, our results may differ from the real

numbers. However, we believe that they are sufficient to understand whether

building and operating a storage facility in Mersin is feasible or not.

CONCLUSION

The

competition for the diesel/gasoil market in MED is getting more eminent among

the major suppliers. As a part of this competition, it is known that

countries like India

and Saudi Arabia are enhancing their refining capacity in order to produce more

diesel/gasoil that can target MED,

particularly Southern Europe and Turkey. With Turkey

being one of the countries with the fastest growing diesel/gasoil demand, Turkey becomes a feasible partner for those countries in

their physical trade of diesel/gasoil to MED. The main challenge in this

competetion against NWE or US is that East of Suez cargoes have to pass

throught Suez Canal. This could cause additional

cost for the cargoes, as well as, delays in voyage times

due to Suez Canal’s heavy traffic.

A

diesel/gasoil storage facility in Mersin seems to be a feasible solution for

these third parties. However, it is important that these countries would have

the ownership of these facilities both in investment and operatorship. This is

critical for two main reasons; firstly, the cost of this facility has to be

covered by the suppliers which are having the majority share of the profit in

this physical trading. Secondly, their operatorship could avoid conflict of

interests among the Turkish local market as none of these countries have a

direct investor in Turkish domestic diesel/gasoil market. As this storage facility is thought to be a

free-zone, so out of Turkish customs zone, then this would make the economics

of this business model work.

Our findings

showed that due to the price differences between Arabian Gulf and Mediterranian if Turkey sells with current prices, it will face losses. However, in the long-run, if Turkey can become a hub for the

region, it will have the power to price

the products according to its interest. Also, becoming a reliable ally for the

energy transportation security, Turkey may increase its political power on the

Eastern Mediterranian, and in the future, it can be a part of the alternative

energy corridor projects. In either case, Turkey’s strong diesel/gasoil demand

and its location creates a good opportunity for Turkey.

In the case where India,

one of the potential suppliers, owns the storage, our findings showed that by

increasing the diesel/gasoil amount that is supplied to Turkey, a storage facility could be operated and the

stored diesel/gasoil can

meet the demands of France

with a more profitable way and the transportation time

will reduce 66%. If the aforementioned case

is not profitable and European countries do not choose to buy from Mersin, the

stored diesel/gasoil can be used domestically as well. The

main purpose of the Mersin diesel/gasoil storage facility is to provide a

promixity to MED market for the East of Suez suppliers

(i.e., Saudi Arabia & India) that they can have a quick access in the OTC

diesel/gasoil market. Especially in contango periods, the storage facility

could create a vital competitive advantage as an oppose to floating storage

operations which are much more expensive than onshore storage options.

The outcome of

the work still relies on much deeper analysis in order to calculate optimum

storage capacity (i.e., Lavera) needed in

Mersin, the average storage fees would apply, the terms for stored

diesel/gasoil could get in Turkish market and the freight economics between Mersin to

Southern Europe which is very limited at the moment. The

capabilities of the participants of these projects are naturally limited to

make these highly complex analysis and calculations. These analysis need to be

done with more data, and in collaboration with counterparties, preferably from

any of the supplier countries, India or Saudi Arabia.

This is also important to understand the business expectations from the suppliers so

that whole project could be mutually profitable. Some of the data such as freight rates are needed for the analysis of this project however

the relevant data could not be found as it is expensive to purchase. This is

another important reason why this project needs to be completed in a much

higher level.

Conclusively,

a diesel/gasoil storage facility for East of Suez products to re-export to MED

sounds like a feasible idea. This could also yield a benchmark price for

Eastern Mediterranean diesel/gasoil market which has a totally different market

dynamics comparing to West Mediterranean. This will be another gain for the

regional countries, especially Turkey, to set their own benchmark prices that

could meet the regional needs. A system that can help East of Suez suppliers (i.e.,

Saudi Arabia & India) that they can by-pass Suez traffic in

sudden high demand periods, which are generally OTC environment, is accepted to

have a good potential and it is worth having deeper analysis.

Disclaimer: There are some certain, and necessary

assumptions have been made throughout the

cost calculation process. We were not able to gather data from some

sources, such as World Scale

Index. We are taking the

vessel Aframax as 70,000 DWT. However,

it can be up to 100,000 DWT. We do not have diesel forward curve prices

for the second month and onwards, so we have estimated

by using the spot and one month forward

prices. Mersin port

costsare overall estimated numbers. They do not represent the true values.

1. Crude Oil

ygu ssever koç

Crude oil is the source of all petroleum products.

Crude oil is classified based on physical characteristics and chemical composition,

using terms such as “light” or “heavy” as well as “sweet” or “sour”. “American

Petroleum Institute (API) gravity is the conventional way of measuring how

heavy or dense a given stream of crude is.” “Crude oil with a low API

gravity is considered as a heavy crude oil and typically has a larger

yield of lower-valued products.”

Crude can also be classified according to

its sulfur content.

Crude oil with low sulfur content is classified as “sweet”, crude oil with a

higher sulfur content is classified as

“sour.” Sulfur content is considered as an

undesirable characteristic with respect to

both processing and end-product quality. Therefore, sweet crude is typically

more desirable and valuable than sour crude. Crude oil varies in price,

usefulness, and environmental impact.

When the crude oil is processed, there

are some specific products that will be

obtained from that specific crude oil (this depends on the natural

quality of the crude oil). Thus, crude oil yield means, depending on the

quality of the crude oil, the high or low valued products obtained as an outcome of the processing. In

this case, same oil may have different

“crude oil yield” for different refineries.

1.1. Crude Oil Processing

Figure 1: Crude Oil Distillates

Lighter crude has a higher percentage of light

hydrocarbons that can be recovered with simple distillation at a refinery.Heavy crude has density approaching or even

exceeding that of water. Usually, heavy

crude requires extra refining to produce more valuable and in-demand products. https://www.thebalance.com/the-basics-of-crude-oil-classification-1182570

Fundamentals of Crude Oil Classification:

1) API gravity measures the density of crude oils.

2) Sulfur content measures the degree of

pureness of crude oil, the level of impurity that each crude oil type contains.

3) Sulfur content higher than 0.5% indicates a

high level of impurity (sour crude oil) that has to be removed.

4) Sulfur content lower than 0.5% implies a low level of impurity

(sweet crude oil).

Due to

the technical points mentioned above, different crude types produce the

products in different yields and quality. Example tables below can be analyzed

to see how the yields of products could change by crude grade, refinery

configuration or region:

Table 1: Arabian

Crude Straight Run Product Streams

|

Light

|

Medium

|

Heavy

|

|

Crude, °API

|

38,80

|

30,70

|

28,20

|

|

Sulfur, % wt

|

1,10

|

2,51

|

2,84

|

|

Light Naphtha

|

|

Cut range, °F

|

68-212

|

68-212

|

68-212

|

|

Yield, % vol

|

10,5

|

9,4

|

7,9

|

|

Gravity, °API

|

77,4

|

78,4

|

80,1

|

|

Sulfur, % wt

|

0,056

|

0,007

|

0,0028

|

|

RVP, Psi

|

6,9

|

7,9

|

10,2

|

|

Paraffins, % vol

|

87,4

|

89,7

|

89,6

|

|

Naphthenes, % vol

|

10,7

|

8,8

|

9,5

|

|

Aromatics, % vol

|

1,9

|

1,5

|

0,9

|

|

RON clear

|

54,7

|

48,2

|

58,7

|

|

Heavy Naphtha

|

|

Cut range, °F

|

212-302

|

212-302

|

212-302

|

|

Yield, % vol

|

9,4

|

7,4

|

6,8

|

|

Gravity, °API

|

58,8

|

59,6

|

60,6

|

|

Sulfur, % wt

|

0,057

|

0,019

|

0,018

|

|

Paraffins, % vol

|

66,3

|

67,8

|

70,3

|

|

Naphthenes, % vol

|

20

|

20,8

|

21,4

|

|

Aromatics, % vol

|

13,7

|

11,4

|

8,3

|

|

Kerosene

|

|

Cut range, °F

|

302-455

|

302-455

|

302-455

|

|

Yield, % vol

|

18,4

|

13,5

|

12,5

|

|

Gravity, °API

|

48

|

48,9

|

48,3

|

|

Sulfur, % wt

|

0,092

|

0,12

|

0,19

|

|

Paraffins, % vol

|

58,9

|

59,9

|

58

|

|

Naphthenes, % vol

|

20,5

|

21,9

|

23,7

|

|

Aromatics, % vol

|

20,6

|

18,2

|

18,3

|

|

Freeze Point, °F

|

-67

|

-72

|

-84

|

|

Smoke Point, mm

|

26

|

23

|

26

|

|

Luminometer no.

|

57

|

55

|

60

|

|

Aniline Point, °F

|

133

|

139

|

138

|

|

Kin cSt at -30 °F

|

5,09

|

4,63

|

4,74

|

|

Kin cSt at 100 °F

|

1,13

|

1,09

|

1,12

|

|

Light Gas Oil

|

|

Cut range, °F

|

455-650

|

455-650

|

455-650

|

|

Yield, % vol

|

21,1

|

17,4

|

16,4

|

|

Gravity, °API

|

37,3

|

37,2

|

35,8

|

|

Sulfur, % wt

|

0,81

|

1,09

|

1,38

|

|

Pour Point, °F

|

10

|

0

|

5

|

|

Aniline Point, °F

|

166

|

156

|

156

|

|

Kin cSt at 100 °F

|

3,34

|

3,15

|

3,65

|

|

Kin cSt at 210 °F

|

1,32

|

1,22

|

1,4

|

|

Heavy Gas Oil

|

|

Cut range, °F

|

650-1049

|

650-1049

|

650-1049

|

|

Yield, % vol

|

30,6

|

30,5

|

26,3

|

|

Gravity, °API

|

24,8

|

322

|

21,8

|

|

Sulfur, % wt

|

1,79

|

2,87

|

2,88

|

|

Pour Point, °F

|

100

|

75

|

90

|

|

Aniline Point, °F

|

195

|

172

|

172

|

|

Kin cSt at 100 °F

|

49

|

62,2

|

62,5

|

|

Kin cSt at 210 °F

|

65,65

|

7,25

|

7,05

|

|

Atmosferic

residue

|

|

Cut range, °F

|

650+

|

650+

|

650+

|

|

Yield, % vol

|

38

|

50

|

53,1

|

|

Gravity, °API

|

21,7

|

14,4

|

12,3

|

|

Sulfur, % wt

|

2,04

|

4,12

|

4,35

|

|

Pour Point, °F

|

75

|

55

|

55

|

|

Con Carb. %wt

|

4,5

|

10

|

13,2

|

|

Kin cSt at 100 °F

|

146

|

1570

|

5400

|

|

Kin cSt at 210 °F

|

12,4

|

54

|

106

|

|

Vacuum Residue

|

|

Cut range, °F

|

1049+

|

1049+

|

1049+

|

|

Yield, % vol

|

7,4

|

19,5

|

26,8

|

|

Gravity, °API

|

11,5

|

3,8

|

4

|

|

Sulfur, % wt

|

3

|

5,85

|

5,6

|

|

Pour Point, °F

|

80

|

120

|

120

|

|

Con Carb. %wt

|

19

|

22,8

|

12,4

|

|

Kin cSt at 210 °F

|

392

|

19335

|

13400

|

Source: Handbook of Petroleum Processing

Table 2: Typical Products Made from a

42-Gallon Barrel of Refined Crude Oil in the U.S.

|

Products

|

Amount

|

|

Asphalt

|

3%

|

|

Liquefied Petroleum

|

4%

|

|

Jet Fuel

|

10%

|

|

Other Products

|

18%

|

|

Diesel Fuel & Heating Oil

|

23%

|

|

Gasoline

|

47%

|

Source: Canary USA (Other products (the 18%) include

chemical feedstocks (for plastics, fertilizers

etc.), lubricants.)

Table

3:

Mediterranean Crude Oil Yields of Refinery Configuration

|

Mediterranean

Yields

|

|

Harmonized

System

|

Harmonized

System

|

High conversion

VGO hydrocracker/Visbreaker

|

High conversion

VGO hydrocracker/Visbreaker

|

|

Volume % Yield

|

Es Sider

|

Urals

|

Es Sider

|

Urals

|

|

LPG

|

2,37%

|

4,41%

|

3,96%

|

5,75%

|

|

Gasoline

|

19,27%

|

13,06%

|

23,65%

|

19,97%

|

|

Naphtha

|

0,00%

|

0,00%

|

0,00%

|

0,00%

|

|

Kerosene

|

7,37%

|

7,60%

|

13,67%

|

14,04%

|

|

Diesel

|

31,90%

|

30,10%

|

40,74%

|

42,80%

|

|

HSFO

|

0,00%

|

41,85%

|

0,00%

|

16,34%

|

|

LSFO

|

35,74%

|

0,00%

|

15,01%

|

0,00%

|

Source: Handbook of Petroleum Products

Table

4: NWE Crude

Oil Yields of Refinery Configuration

|

North West

European Yields

|

|

Harmonized System

|

Harmonized System

|

Fluid Catalytic Cracker+Visbreaker

|

Fluid Catalytic Cracker+Visbreaker

|

|

Volume % Yield

|

Brent

|

Urals

|

Brent

|

Urals

|

|

LPG

|

4,14%

|

4,41%

|

6,42%

|

6,41%

|

|

Gasoline

|

20,85%

|

13,06%

|

34,60%

|

27,11%

|

|

Naphtha

|

0,00%

|

0,00%

|

0,00%

|

0,00%

|

|

Kerosene

|

7,29%

|

7,60%

|

13,40%

|

9,18%

|

|

Diesel

|

32,31%

|

30,10%

|

34,03%

|

37,24%

|

|

HSFO

|

0,00%

|

41,85%

|

0,00%

|

17,53%

|

|

LSFO

|

32,00%

|

0,00%

|

8,99%

|

0,00%

|

Source: Handbook of Petroleum Products

Table

5: Singapore

Crude Oil Yields of Refinery Configuration

|

Singapore

Yields

|

|

Harmonized System

|

Harmonized System

|

Harmonized System/ Fluid Catalytic

Cracker+Visbreaker

|

Harmonized System/ Fluid Catalytic

Cracker+Visbreaker

|

|

Volume

% Yield

|

Dubai

|

Tapis

|

Dubai

|

Tapis

|

|

LPG

|

2,52%

|

1,77%

|

4,10%

|

4,14%

|

|

Gasoline

|

10,05%

|

17,02%

|

19,52%

|

26,04%

|

|

Naphtha

|

6,50%

|

6,08%

|

6,50%

|

6,08%

|

|

Kerosene

|

12,41%

|

20,99%

|

13,46%

|

23,42%

|

|

Diesel

|

22,98%

|

28,93%

|

37,44%

|

36,79%

|

|

HSFO

|

42,26%

|

0,00%

|

15,63%

|

0,00%

|

|

LSFO

|

0,00%

|

21,22%

|

0,00%

|

0,37%

|

Source: Handbook of Petroleum Products

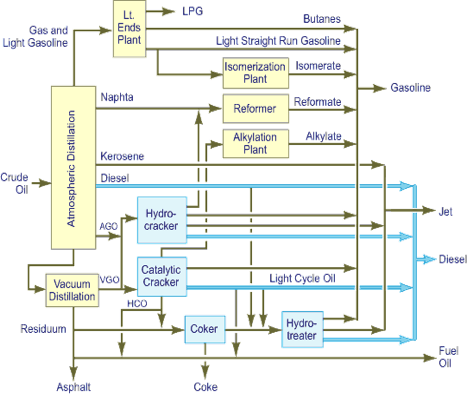

Figure 2: Stages of Crude Oil Refinery Process

VIDEO: Refining is the transformation operation

allowing us to obtain many products that market demands. Depending on the crude

oil’s quality, four main operations are

done to process crude oil. These are; separation,

conversion, improvement and mixing. The crude oil is processed in the distillation oven which the

petroleum products have different boiling temperatures from lightest on the top

and the heaviest on the bottom. The lightest is

LPG (butane and propane), and then comes petrol (for an automobile) and naphtha. From naphtha’s processing, we obtain

olefins and aromatics. On the bottom, we obtain kerosene (aircraft fuel and

domestic heating fuel) and then comes diesel (for diesel engines). Lastly, we

obtain paraffin, lubricating oils, and heavy fuels (production of industrial

heat).

2. Diesel/gasoil

Diesel/gasoil is a type

of middle distillate fuel (light, middle and heavy distillates

have different characteristics where their functions and markets are also

different).

“Diesel fuel is more efficient than

gasoline because it contains 10% more energy per gallon than gasoline.” However, there arefew kinds of diesel/gasoil

fuel. Just as gasoline is rated by its octane,

diesel fuel is rated by its cetane, which indicates how easy

it is to ignite and how fast it burns.

2.1. Main Usage of Diesel

Table 6: Key Consuming Sectors of Diesel Sector-Wise Diesel

Consumption in USA, 2016

|

|

|

|

|

KEY CONSUMING SECTORS OF

DIESEL

|

|

SECTOR-WISE DIESEL

CONSUMPTION (USA)

|

|

Name of the sector

|

Diesel consumption

|

|

|

|

Trucks

|

27.8%

|

|

|

|

Agriculture

|

12.2%

|

|

|

|

Personal SUVs and cars

|

12.1%

|

|

|

|

Buses

|

9.9%

|

|

|

|

Commercial taxis

|

8.3%

|

|

|

|

Three wheelers

|

6.2%

|

|

|

|

Industry

|

6.2%

|

|

|

|

Generation sets

|

3.9%

|

|

|

Railways

|

3.8%

|

Bulk

|

|

Mobile towers

|

1.7%

|

consumers

|

|

Aviation and shipping

|

0.8%

|

|

|

Others

|

7.1%

|

|

|

|

|

|

|

|

|

|

Source: Parasadenwala

3. Trade for diesel/gasoil

The following data is derived by using Joint Organizations Data

Initiative (JODI). In consumption calculation, stock changes are also included. All tables are ordered according to highest 2017H2 values.

Table 7: Major

Output in Diesel (Thousand Barrels)

|

Total Diesel Output (Thousand Barrels)

|

|

Country Name

|

H1 2016

|

H22016

|

H12017

|

H22017

|

|

United States

of America

|

144,814

|

152,221

|

146,724

|

151,222

|

|

China

|

104,318

|

108,709

|

107,839

|

113,181

|

|

India

|

62,445

|

64,692

|

64,247

|

70,631

|

|

Russian

Federation

|

46,457

|

47,872

|

47,007

|

48,370

|

|

Saudi Arabia

|

32,397

|

31,525

|

31,687

|

33,777

|

|

Germany

|

27,918

|

29,239

|

27,452

|

29,536

|

|

Korea

|

28,169

|

28,724

|

28,491

|

29,488

|

|

Japan

|

27,613

|

28,720

|

27,650

|

29,225

|

|

Canada

|

17,901

|

18,573

|

19,760

|

20,649

|

|

Italy

|

19,180

|

21,100

|

19,042

|

17,582

|

|

France

|

14,780

|

17,425

|

15,498

|

17,195

|

|

Spain

|

15,841

|

17,240

|

16,580

|

17,174

|

|

United Kingdom

|

11,890

|

13,503

|

12,410

|

12,862

|

|

Netherlands

|

11,978

|

11,776

|

12,267

|

11,473

|

|

Belgium

|

7,900

|

7,349

|

7,572

|

8,386

|

Source: JODI Database

Table

8: Major Diesel Importers (Thousand Barrels)

|

Total Diesel Importers (Thousand Barrels)

|

|

Country Name

|

H1 2016

|

H22016

|

H12017

|

H22017

|

|

France

|

13,539

|

13,224

|

13,524

|

13,236

|

|

Germany

|

12,721

|

11,123

|

12,475

|

11,331

|

|

Netherlands

|

11,586

|

11,585

|

10,903

|

10,801

|

|

Turkey

|

8,046

|

7,905

|

7,364

|

10,432

|

|

United Kingdom

|

10,153

|

9,557

|

8,895

|

9,530

|

|

Singapore

|

9,872

|

9,493

|

8,609

|

8,579

|

|

Belgium

|

7,237

|

6,619

|

6,720

|

6,325

|

|

United States

of America

|

5,533

|

4,976

|

4,755

|

4,508

|

|

Italy

|

2,993

|

2,909

|

4,228

|

3,103

|

|

Spain

|

3,300

|

2,570

|

3,296

|

2,805

|

|

Saudi Arabia

|

6,058

|

7,289

|

3,424

|

2,009

|

|

Greece

|

621

|

790

|

617

|

814

|

|

Canada

|

1,054

|

786

|

810

|

808

|

|

Bulgaria

|

492

|

675

|

620

|

592

|

|

India

|

1,076

|

129

|

1,334

|

418

|

Source: JODI Database

Table

9: Major Diesel Exporting Countries in the World

(Thousand Barrels)

|

Total Diesel

Expors (Thousand Barrels)

|

|

Country Name

|

H1 2016

|

H22016

|

H12017

|

H22017

|

|

United States of America

|

35,798

|

36,480

|

40,055

|

43,959

|

|

Russian Federation

|

31,465

|

28,291

|

33,173

|

24,377

|

|

Saudi Arabia

|

17,568

|

17,310

|

16,469

|

20,317

|

|

India

|

15,699

|

18,446

|

15,855

|

20,286

|

|

Netherlands

|

18,389

|

18,742

|

18,770

|

18,465

|

|

Singapore

|

14,621

|

15,211

|

15,012

|

15,497

|

|

Korea

|

14,435

|

14,763

|

14,196

|

15,100

|

|

China

|

7,911

|

10,618

|

9,605

|

11,181

|

|

Belgium

|

7,258

|

7,231

|

7,504

|

7,857

|

|

Japan

|

4,928

|

5,344

|

4,685

|

6,220

|

|

Italy

|

5,456

|

6,235

|

6,039

|

6,089

|

|

Germany

|

5,743

|

6,036

|

5,655

|

5,714

|

|

Spain

|

2,535

|

4,024

|

3,666

|

4,452

|

|

Greece

|

4,358

|

4,773

|

4,778

|

4,088

|

|

Canada

|

4,816

|

3,592

|

5,087

|

4,045

|

Source: JODI Database

Table 10: Major Diesel Consumers in the World (Thousand

Barrels)

|

Major Diesel

Consumers (Thousand Barrels)

|

|

Country Name

|

H12016

|

H12016/Per Capita

|

H22016

|

H22016/Per Capita

|

H12017

|

H12017/Per Capita

|

H22017

|

H22017/Per Capita

|

Population

|

|

United States of America

|

112,622

|

0.035%

|

123,438

|

0.038%

|

109,008

|

0.033%

|

107,204

|

0.033%

|

325.7

|

|

China

|

97,558

|

0.007%

|

96,516

|

0.007%

|

99,057

|

0.007%

|

102,029

|

0.007%

|

1,379

|

|

India

|

47,945

|

0.004%

|

46,627

|

0.004%

|

49,677

|

0.004%

|

50,390

|

0.004%

|

1,324

|

|

Germany

|

35,710

|

0.043%

|

34,070

|

0.041%

|

33,526

|

0.041%

|

34,566

|

0.042%

|

82.67

|

|

France

|

26,980

|

0.040%

|

29,827

|

0.045%

|

27,304

|

0.041%

|

28,804

|

0.043%

|

66.90

|

|

Russian Federation

|

15,241

|

0.011%

|

19,705

|

0.014%

|

14,083

|

0.010%

|

23,868

|

0.017%

|

144.30

|

|

Japan

|

22,885

|

0.018%

|

23,633

|

0.019%

|

23,232

|

0.018%

|

23,075

|

0.018%

|

127.00

|

|

United Kingdom

|

18,946

|

0.029%

|

20,250

|

0.031%

|

18,997

|

0.029%

|

19,882

|

0.030%

|

65.64

|

|

Canada

|

13,563

|

0.037%

|

15,999

|

0.044%

|

15,495

|

0.043%

|

17,331

|

0.048%

|

36.29

|

|

Turkey

|

13,637

|

0.017%

|

14,499

|

0.018%

|

14,018

|

0.018%

|

16,678

|

0.021%

|

79.51

|

|

Spain

|

16,801

|

0.037%

|

15,245

|

0.033%

|

15,896

|

0.035%

|

15,215

|

0.033%

|

45.56

|

|

Saudi Arabia

|

20,459

|

0.063%

|

22,182

|

0.069%

|

18,730

|

0.058%

|

15,153

|

0.047%

|

32.28

|

|

Italy

|

17,063

|

0.028%

|

18,086

|

0.030%

|

17,823

|

0.029%

|

14,491

|

0.024%

|

60.60

|

|

Korea

|

13,941

|

0.027%

|

13,715

|

0.027%

|

14,668

|

0.029%

|

14,391

|

0.028%

|

51.25

|

|

Belgium

|

8,103

|

0.071%

|

6,088

|

0.054%

|

6,134

|

0.054%

|

6,329

|

0.056%

|

11.35

|

Source: JODI Database

3.1 Major Players in Diesel Market

This section provides information for the

countries that are the main players in

the diesel market. To show an example, we

started with Russian Federation. We have managed to collect every information

we gather so far to have a better understanding. We intend to expand this

analysis to every country that is relevant to this project. To the best of our

knowledge on the topic improves we will update each section and at the end, we hope that this study will help on

deciding whether Turkey can play a better

role in this market or not.

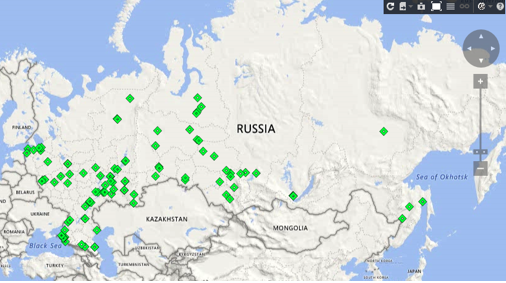

3.1.1 Russian Federation

Figure

3: Overall Refineries in Russian

Federation

Source: Thomson

Reuters Eikon

Russian Federation was the largest diesel

exporter for Europe in 2017. Above m where the Russian refineries are located. Names of those refineries and their

capacities can be found in Appendix A. Highlighted refineries in the

appendix are the largest Euro 5 standard diesel suppliers. Below can also be found

the locations of the 13 largest refineries (more than 200,000 bpd) to understand the density of the regions.

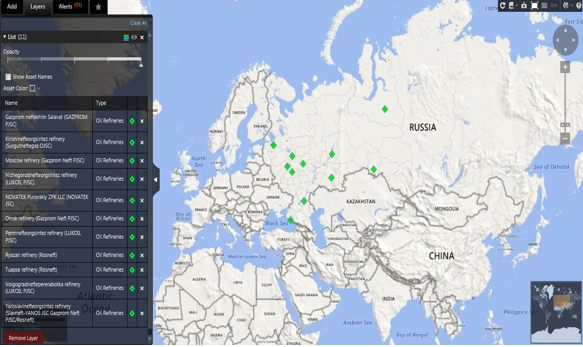

Figure 4: Most Productive Refineries in

Russian Federation

Source: Thomson Reuters Eikon

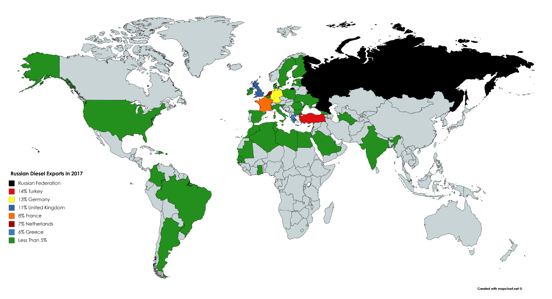

Trade

partners of the Russian Federation can be seen

in the following map. For more information, please

check the table in Appendix B.

Figure 5: Russian Diesel Exports

Source: Thomson

Reuters Eikon

The Russian diesel/gasoil export ports are shown in the following table. According to

these results, both the Black Sea and Baltic Sea have almost equal

importance.

Table 11: Russian Diesel Exports by Ports

in 2017

|

Russian

Diesel Exports by Sea in 2017 (Million Barrels)

|

|

Black Sea

|

Baltic Sea

|

Barents

Sea

|

|

|

Total Exp.

|

Share in Total

|

|

Total Exp.

|

Share in Total

|

|

Total Exp.

|

Share in Total

|

|

Novorossiysk

|

59.01

|

25,81%

|

Primorsk

|

72.46

|

31,65%

|

Murmansk

|

3.28

|

1,43%

|

|

Tuapse

|

40.52

|

17,70%

|

Vysotsk

|

24.88

|

10,87%

|

|

|

|

|

Kavkaz

|

6.26

|

2,73%

|

St.Petersburg

|

12.01

|

5,24%

|

|

|

|

|

Taman

|

2.20

|

0,96%

|

Ust-Luga

|

3.47

|

1,52%

|

|

|

|

|

Azov

|

0.61

|

0,27%

|

Baltiysk

|

2.76

|

1,20%

|

|

|

|

|

Rostov-on-Don

|

0.23

|

0,10%

|

Kaliningrad

|

0.95

|

0,41%

|

|

|

|

|

Taganrog

|

0.13

|

0,06%

|

|

|

|

|

|

|

|

Temryuk

|

0.07

|

0,03%

|

|

|

|

|

|

|

|

Volgograd

|

0.04

|

0,02%

|

|

|

|

|

|

|

|

Total

|

109.15

|

47,67%

|

Total

|

116.52

|

50,89%

|

Total

|

3.28

|

1,43%

|

|

|

|

|

|

|

|

|

|

|

|

Source: Thomson

Reuters Eikon

Also since Russia has a rough climate, we have checked

whether there is any seasonality in diesel/gasoil loadings due to weather

conditions. The results show that there are no significant limitations.

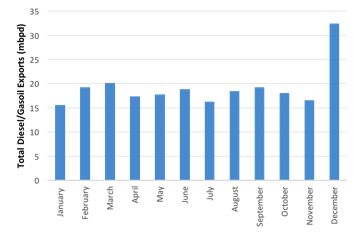

Figure 6: Russian

Diesel/Gasoil Exports by Months in 2017 (Thousand Barrels/day)

Source: Thomson

Reuters Eikon

Table 13: Netherlands Diesel/Gasoil Imports

by Ports in 2017

|

Dutch

Diesel Imports by Ports 2017 (Million Barrels/day)

|

|

|

Total

Imports

|

Share in

Total

|

|

Rotterdam

|

40.80

|

52,79%

|

|

Amsterdam

|

34.25

|

44,33%

|

|

Vlissingen

|

1.80

|

2,32%

|

|

Terneuzen

|

0.36

|

0,46%

|

|

Moerdijk

|

0.051

|

0,07%

|

|

Dordrecht

|

0.020

|

0,03%

|

|

TOTAL

|

77.26

|

100,00%

|

Source: Eikon

Table 14: Netherlands Diesel/Gasoil Exports

by Ports in 2017

|

Dutch Diesel Exports by

Ports 2017 (Million Barrels/day)

|

|

|

Total Exports

|

Share in Total

|

|

Rotterdam

|

41.5

|

69,38%

|

|

Amsterdam

|

17.79

|

29,74%

|

|

Vlissingen

|

0.41

|

0,70%

|

|

Terneuzen

|

0.059

|

0,10%

|

|

Sluiskil

|

0.041

|

0,07%

|

|

Delfzijl

|

0.009

|

0,02%

|

|

TOTAL

|

59.81

|

100%

|

Source: Eikon

Table 15: Russian Diesel Exports to Turkey

by Ports in 2017

|

Russia Diesel Exports to

Turkey by Ports in 2017

|

|

Port Name

|

Total

Exports

|

Region

|

|

Novorossiysk

|

23.65

|

Black Sea

|

|

Tuapse

|

6.30

|

Black Sea

|

|

Kavkaz

|

1.15

|

Black Sea

|

|

Taman

|

0.75

|

Black Sea

|

|

Azov

|

0.18

|

Black Sea

|

|

Rostov-on-Don

|

0.05

|

Black Sea

|

|

Volgograd

|

0.04

|

Black Sea

|

|

Total

|

32.14

|

Black Sea

|

Source: Thomson

Reuters Eikon

Table 16: Diesel/Gasoil Imported from

Russia by Discharge Ports in 2017

|

Diesel/Gasoil Imported from Russia By

Discharge Ports in 2017

|

|

Port Name (Turkey)

|

Total

Imports

|

Share

in Total

|

|

Marmara Ereğlisi

|

7.35

|

23%

|

|

Gebze

|

5.47

|

17%

|

|

Samsun

|

4.18

|

13%

|

|

Tutuncifilik

|

3.70

|

12%

|

|

Aliaga

|

2.95

|

9%

|

|

Trabzon

|

2.28

|

7%

|

|

Mersin

|

2.26

|

7%

|

|

Antalya

|

0.87

|

3%

|

|

Yarimca

|

0.65

|

2%

|

|

Toros Terminal (Ceyhan)

|

0.53

|

2%

|

|

Istanbul

|

0.46

|

1%

|

|

Iskenderun

|

0.38

|

1%

|

|

Dortyol Oil Terminal

|

0.33

|

1%

|

|

Izmit

|

0.30

|

1%

|

|

Diliskelesi

|

0.22

|

1%

|

|

Yalova

|

0.10

|

0%

|

|

İzmir

|

0.04

|

0%

|

|

Total

|

32.14

|

100%

|

Source: Thomson

Reuters Eikon

Table 17: Diesel/Gasoil Imports of Turkey from

India by Discharge Ports in 2017

|

Diesel/Gasoil Imports of

Turkey from India By Discharge Ports in 2017

|

|

Port Name

|

Total Imports

|

Share in Total

|

|

Marmara Ereğlisi

|

8,13

|

62%

|

|

Mersin

|

4,97

|

38%

|

|

Total

|

13,10

|

100%

|

Source: Thomson

Reuters Eikon

Table 18: Diesel/Gasoil Imports of Turkey from

Greece by Discharge Ports in 2017

|

Diesel/Gasoil Imports of

Turkey from Greece by Discharge Ports in 2017

|

|

Port Name

|

Total Imports

|

Share in Total

|

|

Mersin

|

1,65

|

25%

|

|

Aliaga

|

1,28

|

19%

|

|

Dortyol Oil Terminal

|

1,12

|

17%

|

|

Marmara Ereğlisi

|

0,69

|

10%

|

|

Nemrut Bay (Izmir satellite port)

|

0,45

|

7%

|

|

Gebze

|

0,36

|

5%

|

|

Tutuncifilik

|

0,35

|

5%

|

|

Izmit

|

0,34

|

5%

|

|

Iskenderun

|

0,20

|

3%

|

|

Antalya

|

0,10

|

1%

|

|

Istanbul

|

0,08

|

1%

|

|

Total

|

6,60

|

100%

|

Source: Thomson

Reuters Eikon

Table 19: Diesel/Gasoil Imports of Turkey from

Bulgaria by Discharge Ports in 2017

|

Diesel/Gasoil Imports of

Turkey from Bulgaria by Discharge Ports in 2017

|

|

Port Name

|

Total Imports

|

Share in Total

|

|

Marmara Ereğlisi

|

1,748

|

21%

|

|

Samsun

|

1,731

|

21%

|

|

Aliaga

|

1,061

|

13%

|

|

Trabzon

|

1,013

|

12%

|

|

Mersin

|

0,731

|

9%

|

|

Antalya

|

0,530

|

6%

|

|

Iskenderun

|

0,390

|

5%

|

|

Gebze

|

0,332

|

4%

|

|

Tutuncifilik

|

0,292

|

3%

|

|

Istanbul

|

0,190

|

2%

|

|

Ceyhan

|

0,150

|

2%

|

|

Dortyol Oil Terminal

|

0,111

|

1%

|

|

Izmit

|

0,089

|

1%

|

|

Nemrut Bay (Izmir satellite port)

|

0,034

|

0%

|

|

Total

|

8,401

|

100%

|

Source: Thomson

Reuters Eikon

According to Thomson Reuters Eikon data, Turkey

imports diesel from Greece and Bulgaria as it is shown in Table 18 and Table 19

respectively. Turkish Energy Market Regulatory also confirms this result.

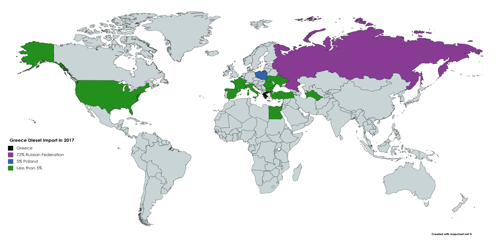

3.1.5. Greece

Figure 13: Diesel/Gasoil Imports of Greece in 2017 by Countries

Source: Thomson

Reuters Eikon

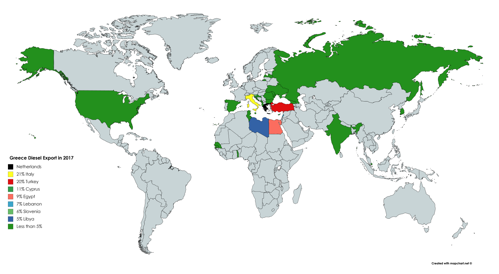

Figure 14: Diesel/Gasoil Exports of Greece

in 2017 by Countries

Source: Thomson

Reuters Eikon

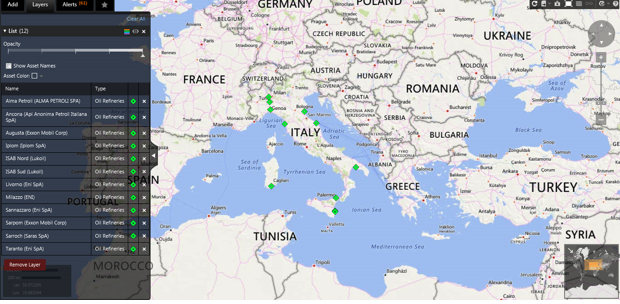

Table 21: Italian Diesel/Gasoil Imports by

Ports in 2017

|

Italian Diesel/Gasoil

Imports by Ports (Million Barrels)

|

|

|

Total Imports

|

Share in Total

|

|

Porto Marghera

|

9.29

|

23,45%

|

|

Genoa

|

6.64

|

16,79%

|

|

Fiumicino

|

5.49

|

13,86%

|

|

Trieste

|

3.57

|

9,01%

|

|

Sarroch (Porto Foxi)

|

3.04

|

7,68%

|

|

Santa Panagia Bay

|

2.21

|

5,59%

|

|

Augusta

|

2.18

|

5,50%

|

|

Gaeta

|

1.18

|

2,98%

|

|

Naples

|

1.17

|

2,95%

|

|

Leghorn

|

1.08

|

2,72%

|

|

Ancona

|

1.04

|

2,62%

|

|

Torre Annunziata

|

0.85

|

2,15%

|

|

Venice

|

0.44

|

1,10%

|

|

Ravenna

|

0.42

|

1,05%

|

|

Taranto

|

0.36

|

0,90%

|

|

Brindisi

|

0.30

|

0,77%

|

|

Vado Ligure

|

0.17

|

0,42%

|

|

Milazzo

|

0.10

|

0,26%

|

|

La Spezia

|

0.07

|

0,18%

|

|

TOTAL

|

39.60

|

100,00%

|

Source: Thomson

Reuters Eikon

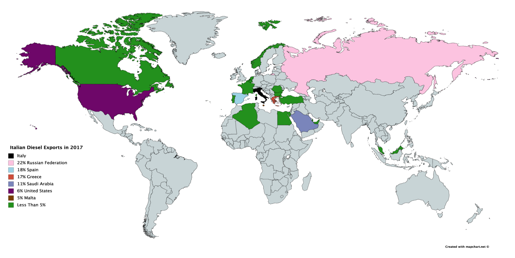

Table 22: Italian Diesel/Gasoil Exports by

Ports in 2017

|

Italian Diesel/Gasoil

Exports by Ports 2017 (in Million Barrels)

|

|

|

Total Exports

|

Share in Total

|

|

Sarroch (Porto Foxi)

|

31.30

|

52,74%

|

|

Santa Panagia Bay

|

16.40

|

27,70%

|

|

Augusta

|

5.74

|

9,68%

|

|

Milazzo

|

1.50

|

2,52%

|

|

Leghorn

|

1.17

|

1,98%

|

|

Genoa

|

1.00

|

1,69%

|

|

Porto Marghera

|

0.78

|

1,32%

|

|

Ancona

|

0.77

|

1,29%

|

|

Ravenna

|

0.33

|

0,55%

|

|

Taranto

|

0.26

|

0,45%

|

|

Vado Ligure

|

0.04

|

0,08%

|

|

TOTAL

|

59.32

|

100,00%

|

Source: Thomson

Reuters Eikon

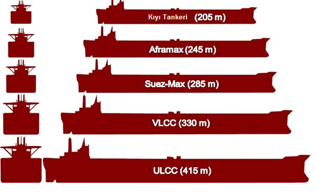

3.2 Vessel Types

The key part of our project relies on the economics of shipping for

physical diesel/gasoil trade. For any particular inter regional path, arbitrage

opportunities occur as long as freight rates would let. So it is vital for us

to understand the dynamics and the economics of diesel/gasoil physical trade

from the East of Suez to MED. This section will focus on understanding these

points.

Cargo ships or

vessels come in different types and sizes to meet the various demands of marine

cargo transportation. Cargo ships are categorised partly by capacity and

partly by dimensions (often related to the different canals and canal locks

they are travelling through). Sizes of

cargo vessels range from a modest handysize carrier

(10,000 – 30,000 DWT) to gigantic VLCC and ULCC supertankers with a capacity to carry cargoes

of more than 200,000 DWT. Aframax and Panamax are

mid-sized cargo vessels.

For clean

products, generally mid-sized cargoes are preferred due to their optimized

costs for clean products cargo sizes. Additionally, their capability to

load/discharge from medium to small size ports make them attractive for clean

products cargoes, as most of these cargoes are loaded from refineries or small

ports close to the refinieries. As an industry fact, majority of the

diesel/gasoil cargoes are carried in Aframax vessels. We preferred to get in

deeper analysis on Aframax vessels based on these abovementioned dynamics.

3.2.1 Aframax

AFRA stands for Average Freight Rate Assessment. As the name

suggests, Aframax is medium-sized oil tankers with a deadweight tonnage (DWT) between 80,000 and 119,999.

Though relatively small in size in comparison to VLCC and ULCC, Aframax tankers

have a capacity to carry up to 120,000

metric tonnes. They are just ideal for short to medium-haul oil trades and are

primarily used in regions of lower crude production

or the areas that lack large ports to accommodate large oil carriers.

3.2.2 Handysize

Handysize are

small-sized ships with a capacity ranging between 15,000 and 35,000 DWT. These

vessels are ideal for small as well as large ports, and so make up the majority

of ocean cargo vessels in the world. They are mainly used in transporting

finished petroleum products and for bulk cargo.

3.2.3 Panamax and New Panamax

As the name suggests, Panamax and New Panamax ships

are travelling through the Panama Canal. They

strictly follow the size regulations set by the Panama Canal Authority, as the

entry and exit points of the Canal are narrow. A Panamax vessel cannot

be longer than 294,13 m (965 ft), wider

than 32,31 m (106 ft) and her draught cannot

be more than 12,04 m (39,5 ft). These vessels have an average capacity of 65,000

DWT and are

primarily used in transporting coal, crude oil and petroleum products.

They operate in the Caribbean and Latin American regions.

The New

Panamax has been

created as a result of the expanding plans for Panama Canal locks.

Expanded locks will be around 427 m (1400 ft) long, 55 m (180 ft) wide and

18,30 m (60 ft) deep so Panama Canal will be able to handle larger vessels.

3.2.4 Suezmax

Suezmax are named after the

famous Suez

Canal. They are mid-sized cargo vessels with a capacity ranging

between 120,000 to 200,000 DWT. They are designed to pass through the majority

of the ports in the world. Currently, the

permissible limits for Suezmax ships are

20,1 m (66 ft) of draught with the beam no wider

than 50 m (164,0 ft), or 12,2 m (40 ft) of draught with a maximum allowed beam of 77,5 m (254 ft).

3.2.5 VLCC and ULCC

VLCC stands for Very Large Crude

Carriers. They have a capacity ranging between 180,000 to 320,000

DWT. They are very flexible in using terminals and can also operate in ports

with depth limitations. VLCCs are used extensively around the North Sea,

Mediterranean and West Africa.

ULCC or Ultra Large Crude

Carriers are

the largest shipping vessels in the world with a size more than 320,000

DWT. Called Super Tankers, ULCCs are used for long-haul oil crude transportation

from the Middle East to Europe, Asia, and

North America.

Figure

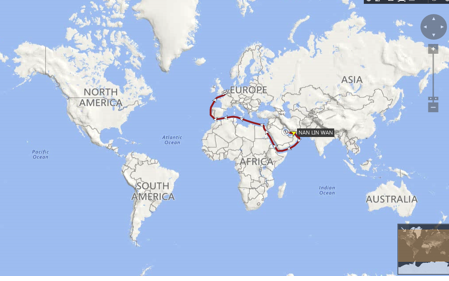

25: Comparison

of Tanker Sizes

Source: https://transportgeography.org

Figure

27: India to

Australia (10 Days)

Source: Thomson

Reuters Eikon

Figure

28: Russia to

Singapore (37 Days)

Source: Thomson

Reuters Eikon

Figure

29: Russia to

Germany (7 Days)

Source: Thomson

Reuters Eikon

Figure

30: the United States to Netherlands (17-18 Days)

Source: Thomson

Reuters Eikon

Figure

31: The United States to France (17-18 Days)

Source: Thomson

Reuters Eikon

Figure

32:

Netherlands to China (50 Days)

Source: Thomson

Reuters Eikon

Figure

33: Saudi

Arabia to the United Kingdom (21 Days)

Source: Thomson

Reuters Eikon

Figure

34: India to the

USA via Mersin (32 Days)

Source: Thomson

Reuters Eikon

Figure

35: India to

Rotterdam (NWE) via Mersin (22 Days)

Source: Thomson

Reuters Eikon

Figure

36: India to

France (MED) via Mersin (17 Days)

Source: Thomson

Reuters Eikon

Figure

37: Saudi Arabia to France(MED) via Mersin (17 Days)

Source: Thomson

Reuters Eikon

Figure

38: Saudi

Arabia to Netherlands (NWE) via Mersin (23 Days)

Source: Thomson

Reuters Eikon

Figure

39: Saudi

Arabia to USA via Mersin (34 Days)

Source: Thomson

Reuters Eikon

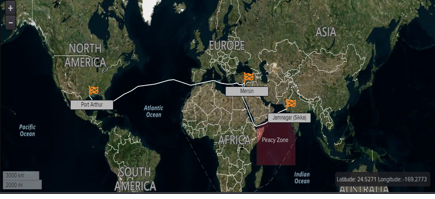

We also provided the information of

the ships that are used in the India –

Turkey – France route in 2017. This information can be useful on understanding

the trade patterns of the vessels. All sources are

taken from Thomson Reuters Eikon, and

total prices are calculated from SeaRates.com

Table

23: STI Rose

Voyages In 2017

|

STI Rose Voyages In 2017

|

|

Load Country

|

Load Port

|

Departure Date

|

Discharge Country

|

Discharge Port

|

Arrival Date

|

Product

|

Volume (kT)

|

Distance

|

Total Price

|

Voyage Time

|

|

India

|

Jamnagar

(Sikka)

|

14.02.2017

|

Egypt

|

Port Said OPL

|

25.02.2017

|

Diesel

|

100,00

|

2.952

|

$705.262,40

|

10

|

|

India

|

Jamnagar

(Sikka)

|

15.03.2017

|

Egypt

|

Port Said OPL

|

25.03.2017

|

Diesel

|

100,00

|

2.952

|

$705.262,40

|

10

|

|

India

|

Jamnagar

(Sikka)

|

16.04.2017

|

Turkey

|

Marmara Erglisi

|

30.04.2017

|

Diesel

|

100,00

|

3.708

|

$890.000,00

|

14

|

|

India

|

Jamnagar

(Sikka)

|

21.05.2017

|

Egypt

|

Port Said OPL

|

01.06.2017

|

Diesel

|

100,00

|

2.952

|

$705.262,40

|

10

|

|

India

|

Jamnagar

(Sikka)

|

19.06.2017

|

Egypt

|

Port Said OPL

|

01.07.2017

|

Diesel

|

100,00

|

2.952

|

$705.262,40

|

10

|

|

India

|

Jamnagar

(Sikka)

|

13.08.2017

|

Egypt

|

Port Said OPL

|

24.08.2017

|

Diesel

|

100,00

|

2.952

|

$705.262,40

|

10

|

|

India

|

Jamnagar

(Sikka)

|

10.09.2017

|

United Kingdom

|

Milford Haven

|

02.10.2017

|

Diesel

|

100,00

|

5.989

|

$1.437.000,00

|

22

|

|

India

|

Jamnagar

(Sikka)

|

26.10.2017

|

Egypt

|

Port Said OPL

|

12.11.2017

|

Jet Fuel

|

97,98

|

2.952

|

$705.262,40

|

10

|

|

India

|

Jamnagar

(Sikka)

|

25.12.2017

|

Turkey

|

Marmara Erglisi

|

10.01.2018

|

Diesel

|

100,00

|

3.708

|

$890.000,00

|

14

|

Source: Thomson

Reuters Eikon

Table

24: Free

Spirit Voyages in 2017

|

Free Spirit Voyages in 2017

|

|

Load Country

|

Load Port

|

Departure Date

|

Discharge Country

|

Discharge Port

|

Arrival Date

|

Product

|

Volume (kT)

|

Distance

|

Total Price

|

Voyage Time

|

|

India

|

Jamnagar (Sikka)

|

28.01.2017

|

Turkey

|

Marmara Erglisi

|

12.02.2017

|

Diesel

|

18,20

|

6.868

|

$873.894,00

|

15

|

|

India

|

Jamnagar (Sikka)

|

04.03.2017

|

Egypt

|

Port Said OPL

|

18.03.2017

|

Diesel

|

90,00

|

2.952

|

$705.262,40

|

14

|

|

India

|

Jamnagar (Sikka)

|

06.04.2017

|

Egypt

|

Port Said OPL

|

18.04.2017

|

Diesel

|

18,20

|

2.952

|

$705.262,40

|

12

|

|

Russian Federation

|

Tuapse

|

02.05.2017

|

South Korea

|

Yeosu (Yosu)

|

04.06.2017

|

Naphtha

|

18,20

|

16.204

|

$3.087.641,00

|

33

|

|

Russian Federation

|

Tuapse

|

02.05.2017

|

South Korea

|

Ulsan

|

26.06.2017

|

Naphtha

|

18,20

|

16.341

|

$3.113.528,00

|

55

|

|

India

|

Jamnagar (Sikka)

|

21.08.2017

|

Israel

|

Ashkelon

|

03.09.2017

|

Diesel

|

50,00

|

3.066

|

$722.145,00

|

13

|

|

India

|

Jamnagar (Sikka)

|

21.08.2017

|

Turkey

|

Mersin

|

08.09.2017

|

Diesel

|

50,00

|

6.122

|

$778.382,00

|

18

|

|

Russian Federation

|

Tuapse

|

21.09.2017

|

South Korea

|

Yeosu (Yosu)

|

30.10.2017

|

Naphtha

|

44,33

|

16.204

|

$3.087.641,00

|

39

|

|

Russian Federation

|

Tuapse

|

21.09.2017

|

South Korea

|

Onsan

|

25.10.2017

|

Naphtha

|

44,33

|

16.340

|

$3.113.528,00

|

34

|

|

Singapore

|

Singapore

|

14.11.2017

|

Turkey

|

Mersin

|

12.12.2017

|

Diesel

|

96,13

|

6.122

|

$778.382,00

|

28

|

|

India

|

Jamnagar (Sikka)

|

31.12.2017

|

Egypt

|

Port Said OPL

|

09.02.2018

|

Diesel

|

51,03

|

2.952

|

$619.157,00

|

41

|

|

India

|

Jamnagar (Sikka)

|

31.12.2017

|

Turkey

|

Mersin

|

14.02.2018

|

Diesel

|

45,10

|

6.122

|

$778.382,00

|

45

|

Source: Thomson

Reuters Eikon

Table

25: Orange

Stars Voyages in 2017

|

Orange Stars Voyages in 2017

|

|

Load Country

|

Load Port

|

Departure Date

|

Discharge Country

|

Discharge Port

|

Arrival Date

|

Product

|

Volume (kT)

|

Distance

|

Total Price

|

Voyage Time

|

|

India

|

Jamnagar (Sikka)

|

02.04.2017

|

Egypt

|

Port Said OPL

|

14.04.2017

|

Diesel

|

50,00

|

2.952

|

$705.262,40

|

11

|

|

India

|

Jamnagar (Sikka)

|

02.04.2017

|

Turkey

|

Mersin

|

20.04.2017

|

Diesel

|

50,00

|

6.122

|

$778.382,00

|

18

|

|

India

|

Jamnagar (Sikka)

|

07.06.2017

|

Turkey

|

Mersin

|

22.06.2017

|

Diesel

|

98,39

|

6.122

|

$778.382,00

|

15

|

|

India

|

Jamnagar (Sikka)

|

11.01.2017

|

Israel

|

Ashkelon

|

25.01.2017

|

Diesel

|

100,00

|

3.066

|

$722.145,00

|

14

|

|

India

|

Jamnagar (Sikka)

|

08.11.2017

|

Turkey

|

Mersin

|

26.11.2017

|

Naphtha

|

46,16

|

6.122

|

$778.382,00

|

18

|

|

Russian Federation

|

Taman

|

14.12.2017

|

South Korea

|

Onsan

|

24.01.2018

|

Naphtha

|

88,85

|

16.340

|

$3.113.528,00

|

42

|

|

Russian Federation

|

Tuapse

|

04.07.2017

|

South Korea

|

Yeosu (Yosu)

|

10.08.2017

|

Naphtha

|

89,99

|

16.204

|

$3.087.641,00

|

36

|

Source: Thomson

Reuters Eikon

Table

26: Abbey Road

Voyages in 2017

|

Abbey Road Voyages in 2017

|

|

Load Country

|

Load Port

|

Departure Date

|

Discharge Country

|

Discharge Port

|

Arrival Date

|

Product

|

Volume (kT)

|

Distance

|

Total Price

|

Voyage Time

|

|

India

|

Vadinar

|

11.02.2017

|

France (Northern)

|

Le Havre

|

08.03.2017

|

Jet Fuel

|

62,99

|

6.023

|

$1.419.297,00

|

25

|

|

Norway

|

Mongstad

|

15.03.2017

|

United Arab Emirates

|

Fujairah

|

08.04.2017

|

Gasoline

|

63,68

|

6.551

|

$3.403.636,00

|

25

|

|

India

|

Jamnagar (Sikka)

|

04.08.2017

|

Netherlands

|

Rotterdam

|

30.08.2017

|

Jet Fuel

|

31,00

|

6.232

|

$1.468.392,00

|

26

|

|

India

|

Jamnagar (Sikka)

|

04.08.2017

|

United Kingdom

|

Thamesport

|

28.08.2017

|

Jet Fuel

|

31,00

|

6.150

|

$1.448.754,00

|

24

|

|

Russian Federation

|

Taman

|

11.10.2017

|

South Korea

|

Yeosu (Yosu)

|

25.11.2017

|

Naphtha

|

57,99

|

8.710

|

$3.074.252,00

|

45

|

Source: Thomson

Reuters Eikon

Table

27: Alpine

Confidence Voyages in 2017

|

Alpine Confidence Voyages in 2017

|

|

Load Country

|

Load Port

|

Departure Date

|

Discharge Country

|

Discharge Port

|

Arrival Date

|

Product

|

Volume (kT)

|

Distance

|

Total Price

|

Voyage Time

|

|

India

|

Jamnagar (Sikka)

|

05.12.2017

|

France

|

Le Havre

|

28.12.2017

|

Jet Fuel

|

94,39

|

6.042

|

$1.423.760,00

|

23

|

|

Lithuania

|

Klaipeda

|

23.06.2017

|

United Arab Emirates

|

Fujairah

|

22.07.2017

|

Gasoline

|

38,63

|

6.730

|

$3.496.470,00

|

28

|

|

Cyprus

|

Limassol

|

17.09.2017

|

South Korea

|

Yeosu (Yosu)

|

17.10.2017

|

Naphtha

|

14,78

|

7.739

|

$2.731.478,00

|

31

|

|

Cyprus

|

Limassol

|

17.09.2017

|

Taiwan

|

Kaohsiung

|

11.10.2017

|

Naphtha

|

14,78

|

6.926

|

$2.229.814,00

|

24

|

|

Russian Federation

|

Taman

|

09.09.2017

|

South Korea

|

Yeosu (Yosu)

|

17.10.2017

|

Naphtha

|

30,95

|

8.710

|

$3.074.252,00

|

38

|

|

Russian Federation

|

Taman

|

09.09.2017

|

Taiwan

|

Kaohsiung

|

11.10.2017

|

Naphtha

|

30,95

|

7.897

|

$2.543.131,00

|

31

|

|

Saudi Arabia

|

Yanbu

|

24.05.2017

|

France

|

Dunkirk

|

07.06.2017

|

Gasoil

|

8,00

|

3.840

|

$2.973.383,00

|

14

|

Source: Thomson

Reuters Eikon

Table

28: Amfitriti

Voyages in 2017

|

Amfitriti Voyages in 2017

|

|

Load Country

|

Load Port

|

Departure Date

|

Discharge Country

|

Discharge Port

|

Arrival Date

|

Product

|

Volume (kT)

|

Distance

|

Total Price

|

Voyage Time

|

|

Netherlands

|

Amsterdam

|

22.09.2017

|

United Arab Emirates

|

Fujairah

|

13.10.2017

|

Gasoline

|

98,09

|

6.095

|

$3.167.086,00

|

21

|

|

Greece

|

Eleusis

|

09.12.2017

|

South Korea

|

Yeosu (Yosu)

|

17.01.2018

|

Naphtha

|

37,74

|

8.074

|

$2.849.306,00

|

38

|

|

Greece

|

Eleusis

|

09.12.2017

|

South Korea

|

Daesan

|

14.01.2018

|

Diesel

|

37,74

|

8.148

|

$2.876.086,00

|

36

|

|

India

|

Jamnagar (Sikka)

|

01.11.2017

|

France (Northern)

|

Le Havre

|

24.11.2017

|

Jet Fuel

|

94,40

|

6.042

|

$1.423.760,00

|

23

|

|

Cyprus

|

Limassol

|

14.12.2017

|

South Korea

|

Yeosu (Yosu)

|

17.01.2018

|

Naphtha

|

11,25

|

7.739

|

$2.731.478,00

|

34

|

|

Cyprus

|

Limassol

|

14.12.2017

|

South Korea

|

Daesan

|

14.01.2018

|

Naphtha

|

11,25

|

7.813

|

$2.757.364,00

|

31

|

|

Singapore

|

Singapore

|

07.08.2017

|

Netherlands

|

Rotterdam

|

10.09.2017

|

Diesel

|

98,09

|

8.298

|

$1.954.881,00

|

34

|

Source: Thomson

Reuters Eikon

Table

29: Ashley

Lady Voyages in 2017

|

Ashley Lady Voyages in 2017

|

|

Load Country

|

Load Port

|

Departure Date

|

Discharge Country

|

Discharge Port

|

Arrival Date

|

Product

|

Volume (kT)

|

Distance

|

Total Price

|

Voyage Time

|

|

Gibraltar

|

Gibraltar

|

24.07.2017

|

France (Northern)

|

Le Havre

|

30.07.2017

|

Jet Fuel

|

96,62

|

1.260

|

$975.655,00

|

6

|

|

India

|

Jamnagar (Sikka)

|

02.03.2017

|

France (Southern)

|

Fos

|

19.03.2017

|

Diesel

|

50,05

|

4.549

|

$1.072.060,00

|

17

|

|

Saudi Arabia

|

Jubail

|

25.08.2017

|

Netherlands

|

Amsterdam

|

26.09.2017

|

Diesel

|

80,00

|

6.528

|

$5.054.127,00

|

31

|

|

Turkey

|

Tutuncifilik

|

11.04.2017

|

|

|

15.04.2017

|

Gasoline

|

80,00

|

|

|

4

|

|

Saudi Arabia

|

Yanbu

|

21.10.2017

|

Belgium

|

Antwerp

|

06.11.2017

|

Diesel

|

80,00

|

3.932

|

$3.044.795,00

|

16

|

Source: Thomson

Reuters Eikon

Table

30: Breezy

Victoria Voyages in 2017

|

Breezy Victoria Voyages in 2017

|

|

Load Country

|

Load Port

|

Departure Date

|

Discharge Country

|

Discharge Port

|